Real value of benefits will be halved in 50 years

by Gareth Morgan on May 19, 2012

Benefit rates are normally increased – uprated – every year in April. Some are frozen at the moment but, we hope, only for a short time.

Until this year they’ve normally been increased by the Retail Prices Index (RPI) using the annual change in the previous September. The idea is that this should allow people to be able to buy the same amount this year that they could the previous year, taking account of rises in prices.

This year the government has changed the way it does it. Instead of using the RPI rate last September it’s using the Consumer Prices Index (CPI) in the same month as the basis for the increases in benefit rates from now on. CPI is normally lower than RPI so benefits get increased by less. This April most benefits increased by 5.2%, the CPI rate in September 2011, instead of 5.6% which was the RPI rate – a difference of 0.4%. Crudely this means that someone who could buy £100 worth of goods last April will now only be able to buy £99.60 worth this year.

That might not seem a huge drop, particularly in generally tough times, but this difference is going to carry on year after year. That means less purchasing power each year compared to the previous year. It’s also going to be more of a drop than 0.4% a year in future. The Office for Budget Responsibility, which is the country’s official body responsible for producing financial forecasts, says that the difference between RPI and CPI will have risen to 2% by 2017 making the yearly drop in purchasing power much bigger (1). In the longer term it thinks that the difference will be about 1.4% (2).

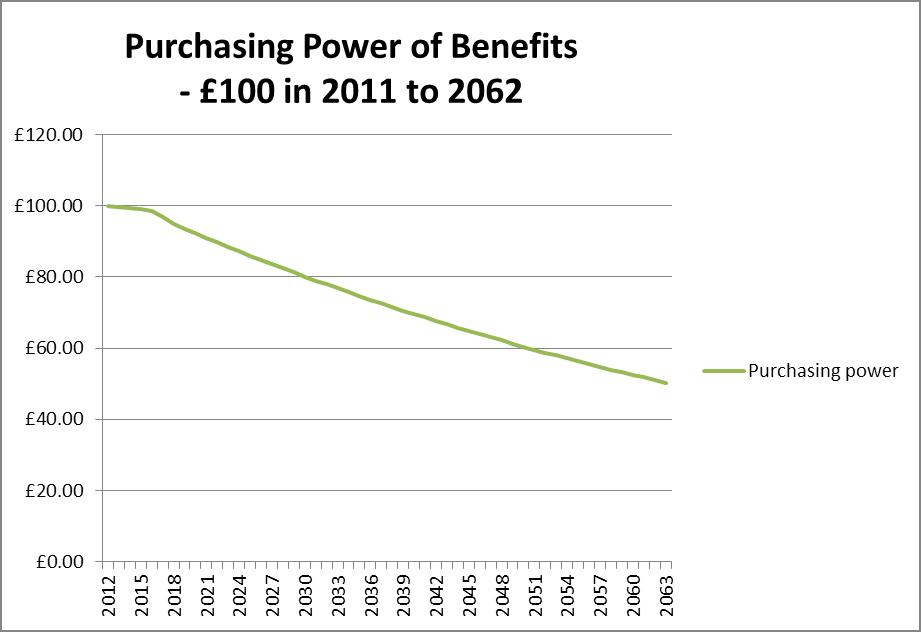

I thought that it would be worth trying to put some values to this reduction rather than just ‘knowing’ that benefits would be gradually nibbled down in real value over time. I took the year by year forecasts for the difference between RPI and CPI given by the OBR up to 2017 and then used their longer term estimate of 1.4% after that. Starting from £100 in April 2011 I reduced the real value, each year, by the forecast difference between RPI and CPI in the previous September. The table below shows the first few years.

| 2011 | 2012 | 2013 | 2014 | 2015 | |

| RPI / CPI difference | 0.40% | 0.40% | 0.40% | 0.70% | |

| Purchasing power | £100.00 | £99.60 | £99.20 | £98.80 | £98.11 |

| reduction | £0.40 | £0.40 | £0.40 | £0.69 |

I extended the calculation to see what would be the real value of benefits, if this link continues, much further into the future. On this basis there are a couple of very worrying markers:

The real value of benefits becomes 10% less in 2020

The real value of benefits becomes 25% less in 2033

The real value of benefits becomes 50% less in 2062

Here’s a chart showing the trend (click on it to see a larger version).

The future value of benefits

The question is; if this government, and those following, continue with this method of indexation, when do benefits fall in real value enough to make life completely unsustainable?

(1) Office for Budget Responsibility, Economic and fiscal outlook March 2012. Cm 8303

(2) Office for Budget Responsibility, Working paper No. 2 – The long-run difference between RPI and CPI inflation, Ruth Miller, November 2011

(ps. My updated paper on Benefits after the Act, with all the new modelling etc. is getting closer – check back in about 10 days).

Comments

I have a question that so far no one seems able to answer and I am hoping that maybe here it can be: the UC rules state that there are circumstances under which an individual can be denied any benefits at all – such as refusal to take an offered job. There are many very valid reasons why someone might feel the need to decline a job offer which have nothing to do with being ‘work shy’. But even if that was the reason, this seems an extreme measure to take. Denial of benefits utterly alienates an individual from society and – effectively – removes them from it. It also leaves no incentive to re-engage. Deductions for non-compliance would seem to me to be much more effective in maintaining an individual’s engagement with and investment in society. I find it disturbing that such sanctions are already being applied within the present system and there are people today forced to get by on zero benefits and zero work.

How is it postulated that these people will survive if they have literally nothing to live on? Has the cost of social-disorder/increased crime been included in the governments calculations?

The UC seems to reflect a ‘let them eat cake’ approach from the government.

This what the government sees as a carrot and stick approach. The carrot is the extra benefit that is paid to those who do work, which, to be fair, for many will be more generous than in the current scheme. The stick is the increasingly harsh ‘conditionality’ which is being imposed on people who do not meet the commitments that they have to enter into for receipt of of benefit. The penalties and sanctions are the first part of the Act to be brought into force.

The government says that people in work have to obey rules and may suffer financial penalties, including loss of pay, if they don’t so people out of work should do the same.

However one feels about the philosophical basis of these arguments your question is fundamental; “how will these people survive”? The government believes that people, faced with these penalties, will follow the rules, or be driven to do so after a short while. Others see this leading, particularly for those whose capability lies at the base of non-compliance, to the black economy, crime and social disorder.

Hello Gareth

Hope you are well.

I have attend a number of your courses recently with regard to benefit changes. I thought you may find it interesting as Tameside MBC has been selected to be a ‘guinea pig’ for the new Universal Benefits. ahead of its launch.

I wondered if you had any advice you could give

thanks and regards

janet Hilton

Michael,A quick observation, as i’m sure you know, the poor die many years bfoere bfoere the rich.A pensioner in Kensington can expect to live well into their 80s, whereas a pensioner from Glasgow might expect to live until their early 70s. This week, we learnt that homeless men have a life expectancy of 47 years. The poorest in our society are unlikely to claim a pension.Pensions are likely to be regressive, simply because the poor die so much younger.So it is either disingenuous or insane to claim that it’s a terrible thing that the poor rely on means tested benefits. Means testing insures that our limited resources are given to pensioners who actually need the state’s help, not to people who don’t. A nice example is the full basic state pension, worth a3135,000 at current annuity rates, given to you and millionaires in the house of lords. I’m not convinced this will do much reduce poverty.Secondly, given how little Brits are currently saving for their retirements, do you really believe that it is a good idea to reduce the incentives for people to save to support themselves during their retirement?Finally, Lord Hutton’s report continued the fine British tradition of making ludicrous assumptions in order to make our public sector pension system appear remotely solvent. Economists and actuaries have been warning about the UKs pensions crisis for at least a decade. Over your long career in politics did you take any steps to insure that our pension schemes (state and public) were sufficiently funded? In short, I’m not convinced you are wise opining about this, given your parties achievements in reforming the UK’s pensions system over the last 15 years.

To day Friday 10 February 2012 the Daily Telegraph front page have a news flash on the older generation. Have we seovld the problem, I think not? It makes for uncomfotable reading.Work until 70+ draw your pensions (State and private) at a minimum age of 70.Rent your house out/ down size (Not sure how)!!This is a loaded situation. Take the house(Literally-It is robbery) down size: How by1 Renting downsize property (The new rent covered by renting out the mortgage free house?) This begs the question the renting of the mortgage free owned property: Is it cheaper for the council/new tenents to pay below market rent values for the house, or is it altruistic dreams to help with the rent of the downsized property rent? What happens when the downsizing has been completed and these persons need welfare and care? Do the council compulsory purchase at the lower vaue of the downsized rent??? Robbery I say.2 Why do not the older persons sell the property for a reasonable market value and downsize into a private or leased property relinguishing all title to the original property? Who stands to gain if it is an amicable solution, or is the market so depressed that expectations are that only a compusory purchase by the local councils is the only solution?? Again is it robbery?? How does one release funds for welfare and care??3 For the older person downsizing to make arrangements and hold tenancy agreements for their property if they rent it out means hassle, and the ability remain business astute and wise until or as they reach the purley gates! Again another expense put on the older person, who has to be able to provide for themselves and spouse/partner, with a roof over their head and the proviso of welfare and care if needed?/ I doubt if this is viable and practical over the age of say 80? Unless you invite family or legal representatives to do the business for you?? Again it is monies spent for who’s benifit.4 We are over retirement age to employ helpers and assistants to help the economic climate of UKPLC.??Some of the ideas are reasonable, but I feel we are all going to hell in a handcart!!!! Answers on a postcard please.